The audience in the large space where auctions are held tends to be tense, excited, curious and worried when an exceptional item is on the stand and the auctioneer is soliciting ever-higher bids. The bidders are usually in the audience, at times making small gestures to express their willingness to up their bid. Other bidders are on the phone with auction house staffers passing their instructions on to the auctioneer. The audience and phone bidders are typically a mix of traders and collectors, who buy with the intention of making a sale in the near future or those who want to hold on to their purchases for a long time, driven by the bottom line or those by their love for the items on the block. Each bidder hopes to make a successful purchase, within their guidelines and budget considerations.

The tension in the bidding room has to do with more than the question: “Will I be able to buy this item?” Some want to see if price records are broken, something that may pull up the price of other items. Anticipation is also felt by a different group of people – those often-anonymous people selling the items. They, too, want to see prices soar. The feeling during the auction when your item is on the podium can be a serious rush.

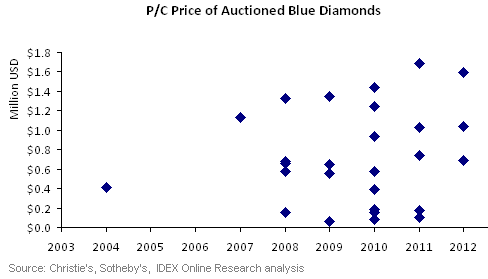

The global press seems mesmerized by record breaking prices of diamonds at auctions, fueling a belief that auctions are the place where prices head up, that if you want to sell a special item, you’ll get the best price at Christie’s or Sotheby’s.

However, the question that must be asked is, as a seller, will you get the largest check at the auction? Further, is there a chance that the way auction houses sell diamonds actually dampens price hikes?

The sales business model

There are two main ways of selling (and buying) an exceptional diamond, the kind we usually associate with investments, the high-end diamonds that fetch hundreds of thousands or millions of dollars: via auctions or dealers.

The auction houses have a great proposition: We bring you the top buyers in the world to one place. The unspoken understanding is that they compete with each other for your diamond – driving up its price in the process. Further, auction results are public, so you know what prices were paid for diamonds similar to yours in the recent past, providing you with a loose realistic expectation of what price your diamond might be sold for.

However, there is more to this. First, the publicized final price includes the buyer’s premium, a fee the buyer pays the auction house. In addition, as a seller, you also pay the auction house a fee, further bringing down the amount of money the seller eventually receives.

At the major auction houses, the buyers’ premium fees ranges from 12 percent to 25 percent, depending on the hammer price – the higher the price, the lower the premium. A hammer price of $1 million has a buyer’s premium fee of about 20%. This can reduce the cash-in-hand considerably below expectations. For example, a diamond sold for $1 million (with the buyer’s premium) has a hammer price of $833,333. From this sum, the auction house collects a 20% fee of $166,666 from the seller, bringing the invoice to $666,667. Not a meager amount of money, yet a third less than the sum that will appear in the auction results publication.

There is no doubt that the auction house deserves payment for its hard work. They have heavy marketing expenses publicizing the auction, including printing a high-cost and well laid-out catalog, bringing top buyers, paying for security and insurance costs and more. From the auction house perspective, to cover its costs it must generate an income, which is the goal after all.

There is an interesting component to an auction: the reserve price. After evaluating the diamond, the auction house sets a reserve price. This promises the seller that their item won’t be sold for too low a price. Nevertheless, it can be a double-edge sword. Seasoned buyers, which many of the buyers are, often say that the reserve price is on the low side, it means that often the bidders don’t rush ahead with their bidding, especially if they are mostly traders.

Does the model put a cap on price?

If collectors heavily populate the audience at an auction, any trader will tell you that there is a good chance that prices will run high. Remember, although savvy and informed, love of diamonds drives collectors, and willingness to pay more reflects this. Traders, on the other hand, always have the next stage in mind, asking themselves, “For how much can I sell the diamond?” Obviously, when the crowd is trader heavy, hammer prices tend to be lower.

When we look at auction results, the headline items, the top, heavily promoted, items are those that catch our attention. But an auction usually offers many additional items. When we consider the auction results, we must look at the prices of all the offered diamonds. While the celebrated items may break record prices, the overall results may tell a somewhat different story.

As traders and seasoned collectors know, sometimes it’s best to play it cool. Understanding that when the reserve price is on the low side, they have the opportunity of buying an outstanding item for a good price. It is a wining proposition: The auction house picks a 33% total fee, and the buyers buy diamonds at a decent price. Is it the best proposition for the seller, or even the diamond investment sector?

If the majority of auctioned diamonds have a reserve price and the majority of buyers buy prudently, then can a low reserve price lead to a low hammer price for the non-headline items? After all, the auction houses are more interested in selling items that come from collectors and inheritances rather then from traders because a trader will pay the auction house just a few percentage points for selling his diamonds.

From the auction house’s position, this is a less lucrative source of diamonds. Traders and non-traders differ in another regard – the amount of on-hand information. Traders specializing in high-end goods are frequently much better informed about current diamond prices than non-traders. Someone selling his grandmother’s large D/FL diamond may be very impressed by a price that does not faze a trader who really knows the current market prices.

There is an alternative route to selling such diamonds – go straight to the trader. Yes, there are some apparent drawbacks, for example, most folks don’t know traders specializing in these goods (or any diamond trader, for that matter). In addition, the allure of an auction and the feeling that a high-selling price is very possible is very tempting. However, any retailer specializing in high-end goods can introduce consumers with a unique item to a serious trader with an excellent reputation. The trader will still want to buy the diamond at a price that will allow a profitable resale, but that margin is much smaller than the 33% paid to an auction house.

Consider the math: If we stick with the $1 million final auction price mentioned earlier, and the trader aims at a 15% margin, he’ll be willing to pay $850,000 for the diamond. This is $183,334 or 27.6% more than the seller will get from the auction house. Even if the trader is uncertain and thinks he’ll get just $900,000 for the diamond, at a 15% margin, he is still willing to pay $765,000 for the diamond. The diamond seller is still a cool $100,000 ahead of what he would get through an auction house. An added bonus is that the trader pays now. With an auction house, you may need to wait a couple months for the auction to take place.

From a seller’s perspective, the downside of dealing with a trader is the feeling that you may have missed out on a wild price at an auction, and the loss of excitement attending the auction. On the upside, a realist does the math and gets a great price. As for the rush, a hundred grand can buy you a lot of adrenaline and some nice champagne to celebrate the windfall.