What a horrible year it was. Miners, traders and retailers will remember 2015 as the year of lost capital, walking on the cusp of bankruptcies, lost opportunities and diminishing value of diamonds. How did it happen, could it been avoided and what lessons can be drawn from it – short term and long?

The last cycle of 2015 – Sight 10 and ALROSA

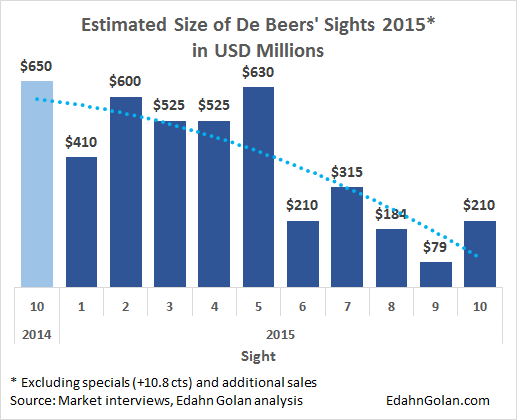

Sight 10, De Beers’ last supply week of the year, had many of the markings of what can and should be done to revive the industry, while at the same time displaying how bad it got and how it may remain problematic.

De Beers reportedly had some $250 million worth of rough diamonds offered in the last cycle. The final tally is estimated at about $210 million worth of rough sold, up an estimated 167% from the previous month and down 68% year-over-year.

The good news: a small Sight with no reported ex-plan or specials (although there may have been some specials offered at the South African Sight). De Beers did not ask or expect Sightholders to meet their ITO commitments that included an estimated $1.5 billion worth of deferred rough goods. The ITO, for all intents and purposes, is out the window.

De Beers has so many goods that it is not mixing refused boxes with the general supply or re-sorting. Instead, for the first time, it offered boxes from Sight 8 and 9 as is. Yet Sightholders could buy only some of the goods they were originally scheduled to receive, as De Beers continues its efforts to reduce the volume of supply to the market. Prices and assortments were unchanged, despite a hope among Sightholders (and an understanding among everyone) that further price reductions are needed.

On the other hand, it must be asked why, at a time when drying up inventories is recognized as an essential step towards reviving the industry, was supply more than double that of Sight 9? The only thing that has really changed since early November is that Diwali is over.

Indian Sightholders bought because of the return from Diwali and their interest in firing up their manufacturing. The point is that demand is still low, as are prices of polished, inventories are still high, and the price discrepancy between rough and polished is such that many boxes still result in a loss. Then why buy goods at all? Many of the Israeli Sightholders, for example, took advantage of the ability to further defer goods and bought next to nothing.

The answer, according to several Indian Sightholders, is that they had no choice. The alternatives are to have workers idly loaf around the factory or to send them home without pay and risk losing them altogether. Either way, these clients chose to buy rough – but focused on the lower cost items.

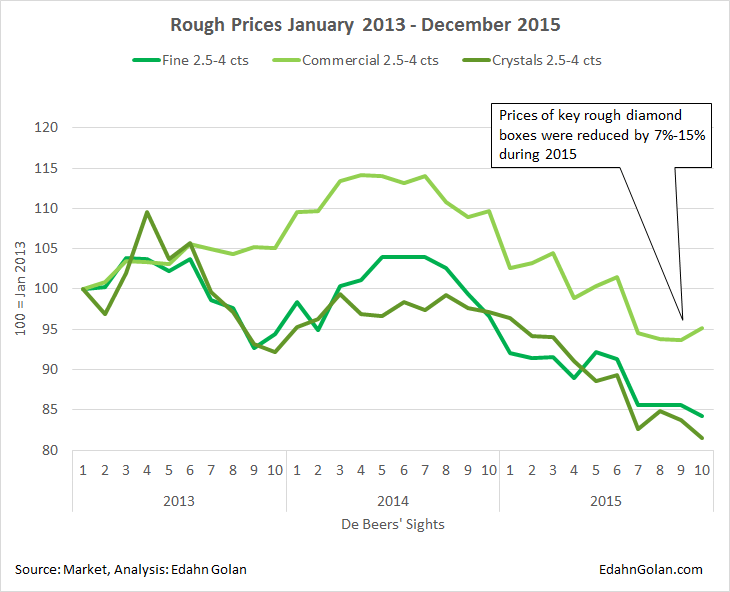

It would be safe to guess that these purchases were not meant to stock up on goods. The general sentiment in the market is that De Beers needs to lower prices by another 10%-15% and that prices will decline in January. This price reduction is not expected to be 15% or even 10%, but rather around 5%-8%.

The bad news: the Sight took place as initial reports from the US and Chinese consumer markets indicate a near flat demand compared to the already weak 2014 holiday season. The requests for ex-plan ahead of Sight 10 and willingness to buy even in areas where there are no shortages are a sign that at least some Sightholders are willing to revert to the proven disastrous practices of buying in near disregard to profitability.

In a way, De Beers cooperated with these Sightholders by offering a relatively large supply at Sight 10, which is not good for the dry up momentum underway.

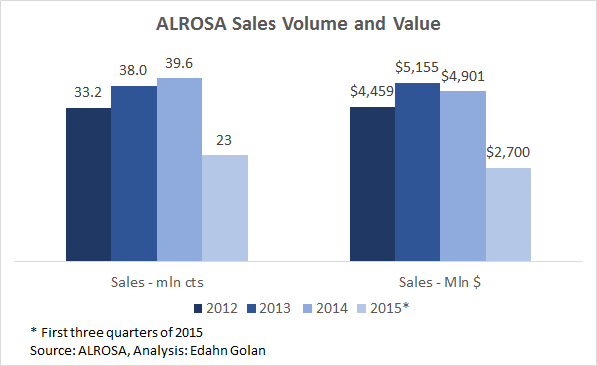

ALROSA has kept prices largely unchanged in December, to the dismay of its clients who want to see the Russian diamond miner further reduce prices. It sweetened the bitter pill by offering all its clients a very low cost parcel to allow for some correction. Still, even with the growing flexibility it too is showing, clients want it to reduce prices to match the current market needs.

De Beers going out of its way

With hardly any trade in the secondary market and premiums at 1% to below box cost, there is no logic in buying for trading or to simply dump unwanted goods. De Beers went out of its way to supply its clients with only what they needed.

Sightholders could replace some of the goods they did not need with other, more useful goods. Another example is the buyback program, where De Beers repurchases goods from Sightholders, which was increased from 10% to 20% a couple of months ago.

There were not many buybacks, yet there are reports in the market that De Beers paid more than usual for some of the goods in this program – enough to make the rest of the box profitable. Further, there are several claims that the miner was even more flexible about it, allowing Sightholders to do this with more than one box and more than 20%. As one insider stated, De Beers is trying to be pragmatic.

ALROSA still expensive

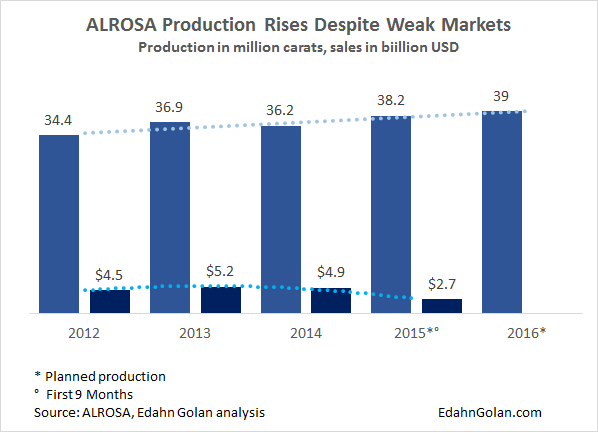

In Moscow, ALROSA seems to be sending mixed messages to its clients. During a client presentation last week, company executives told clients its plans are to keep producing without slowing down despite the industry crisis. That was backed by a statement issued on Tuesday stating that diamond production is expected to be upped to 39 million carats in 2016.

Putting this in perspective, in 2014 ALROSA produced 36.2 million carats, and in the first nine months of 2015, it increased production by 15% to 29.6 million carats with the aim of producing to 38.2 million carats in 2015. Production in the third quarter, when there was absolutely no doubt that we were in the midst of a crisis, was actually accelerated compared to the first half of the year when production was up 13%.

That said, in private discussions ALROSA executives stated that they may not increase production completely out of tune with sales. The official sales goal for 2016 is also ambitious. According to the company, rough diamond sales in 2016 are planned to total $3.5 billion “taking into account a minimal demand growth.” This is close to the estimates for their sales in 2015.

However, ALROSA is facing a different issue altogether. After reducing prices by an estimated 20%, their contracted clients still state that ALROSA is pricing its rough too high and further reductions is needed. The company may address this issue through changes to its contracted sales system, already quietly admitting that their current allocation system is not working well, especially in hard times.

The way to address this could be by stepping away from standard assortment mixes and creating what one of their clients called “tailored” assortments. For starters, it would be difficult to compare prices over time and so discourage talk of being expensive. Also, it would allow the company to reduce prices discreetly and to fit their offerings more accurately to market needs.

The lost year

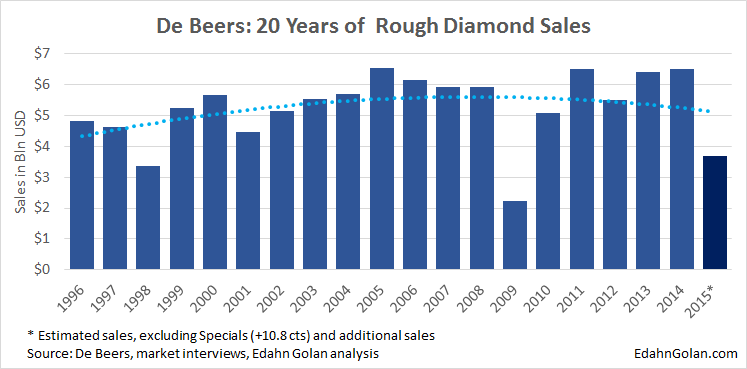

Taking a longer view of the year, it is clear that the bullwhip effect that started with inventory buildup among retailers in the main markets – the US, China, India and Japan – resulted in a buildup in inventories in the manufacturing section of the diamond pipeline.

A faster response on the part of miners could have prevented a further detrition of the situation or could have at least mitigated some of it. However, the drive to perform on a quarter-by-quarter basis led De Beers’ CEO to make the ill-fated statement that it’s up to him to take care of De Beers’ bottom line and up to the Sightholders to take care of theirs.

While that may be true, it proved shortsighted as the company saw sales drop 21% in the first half of the year and take a potentially disastrous dip in the mid-term. Sightholder sentiment was not just negative – it was downright contrary. Every time a Sight ended with a high level of refusals, Sightholders chuckled vindictively. This was clearly not an atmosphere conducive to doing business.

De Beers, as noted above, realized that it could not simply pump diamonds into the market and dump responsibility on the midstream – it had to take action. After all, as the rate of diamond companies calling it quits – through bankruptcies, quiet closures or by simply shutting down operations such as polishing facilities in Botswana – has only increased, the company had to make sure it’s not sawing off the branch it is sitting on.

Yet it started taking steps and initiatives in earnest only in the second half of the year. We could argue that 2015 was the year of carrying 2014 mistakes. Producers ignored the high inventories and continued to pump rough into the market. If they would have reduced prices and volume early enough – instead of the price hikes – 2015 would have looked very different.

Miners had it bad

Not only did diamonds take a hit this past year, but the entire mining sector fell as the Chinese economy lost some of its steam. From an investors’ perspective, mining is a lot less attractive, and diamond miners especially so. According to commodities and mining sector analyst Kieron Hodgson, the lack of diamond price transparency makes them difficult to judge and therefore investors are hesitant to pump money into the sector.

On the upside, the large number of special diamonds found by miners in the past year had a casino-like quality – a chance to win big. This is something investors may like; otherwise, the relative stability of diamond prices compared to other commodities makes diamonds seem a bit boring.

What 2016 has in store

It is too early to predict when the market will improve. It will have to include continued reduced rough prices, stabilized polished diamond prices and drying up of diamond inventories along the pipeline, especially among manufacturers, who are already down by about 20-30% since the start of the year according to one Sightholder.

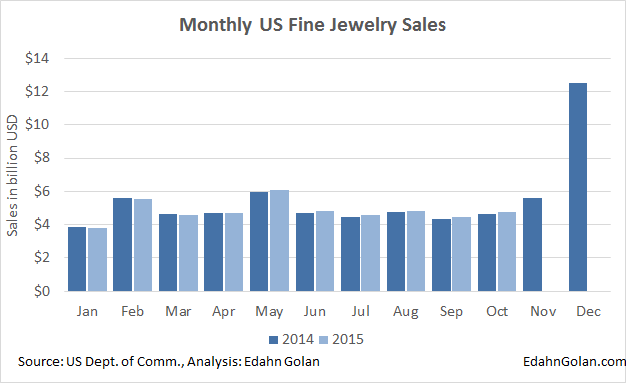

Most importantly, it will require a revival of the consumer market. The signs are not fully there yet. In the first ten months of the year, overall jewelry sales in the US increased by a meager 0.8%, barely beating the inflation rate. For all intents and purposes, jewelry sales are flat with the poor sales of last year.

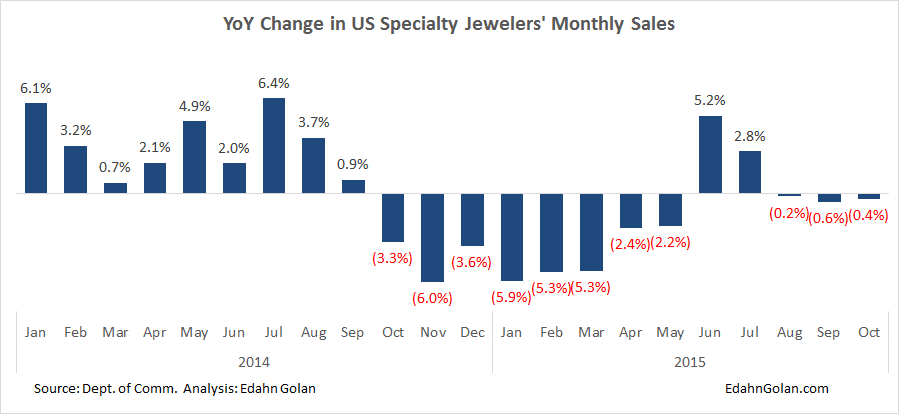

For specialty jewelers alone – where diamond sales are more interesting, both in overall value and per item – sales were still lagging behind in October. Reports from the market suggest that the bigger chains are doing alright – with sales up 3%-5% compared to last year. The rest of the many independents are suffering from a less than cheerful holiday season.

A finer look will show that although overall jewelry sales were poor in the first four months of the year, they have improved since May and can end the year positively. However, that is not the scenario specialty jewelers are facing. The slow year stretched into May, improved in June and July and sank again in August–October.

Financing still an issue

It is important to remember that alongside the decline in consumer purchases, the main complaint by many in the industry was in regard to financing. The financing crunch was a result of continued rough diamond purchases alongside polished diamond slowing sales.

The midstream gets much of its bank financing against sales invoices to prove cash flow and viability. Therefore, the continued rough buying expenditures while cash flow is dwindling exasperated the financial woes and banks’ worries.

While today most are focusing on high rough prices, dwindling consumer demand and low polished diamond prices, financing problems are still looming in the background. High interest rates and a tendency to tighten credit supply are issues that will jump front and center when matters improve – whenever that happens.

Miner uncertainties

Rough diamond prices just have to come down. The discrepancies in price are still there, and manufacturers’ profitability has to be restored. A 20% price reduction is too harmful and will erase too much value. A 5% reduction is enough to buy, but will not restore profitability. However a 10% reduction will allow both profitability and balance.

The question is how to do it. A sharp one-time reduction creates an uneasy feeling among most. One reason is the concern that it may result in a dash for goods. According to a few industry members, the price reductions should happen in a couple of stages – in January and again in February – and should be discrete.

A change in assortments that makes box price comparison impossible is one way of doing this. That would go along with what ALROSA is entertaining already, and maybe De Beers as well. Further, if the two reduce prices by 10% and keep volumes low in 2016, then we can expect an improvement in the market.

Is better truly better?

No, this is not a Zen question, but a practical one. Once diamond jewelry retail sales are revived, we may see another bullwhip effect – this time with the reverse trend of a strong pull coming from downstream climbing upstream. This sudden demand could possibly result in a sudden hike in rough diamond prices.

Many warn of manufacturers returning to old buying habits of buying rough almost regardless of price. It would be a total disaster if it happens. Both miners and manufacturers should be vigilant and act with a long-term view.

For the public mining companies, investor sentiment will continue to be challenging. As mentioned, investors are a lot less interested in mining companies in general. Under- performance and oversupply is standing in the way of price increases, according to Hodgson. A possible outcome could be consolidation.

The perspective of judging a mining company for now is the ability to absorb weaker prices over an extended period of time. Come to think of it, this is true for manufacturers and retailers as well.