Trading on the world diamond market is slowing down after a very successful first quarter. However, this slowdown is not a reason for pessimism. It only means that the diamond market has finally found a point of balance, giving the entire industry a hope for a stable year.

Three months of growth

The results of the first quarter proved to be extremely successful for the entire industry. Demand for diamonds and jewelry, which was markedly low last year, started to recover. Polished goods in the categories of 0.3-1 ct went up in price by 1.4-6% in the first quarter, according to RapNet Diamond Index. Following the increase in demand, diamantaires began to stock up inventories fairly emptied after holiday sales. And mining companies, which earlier expected extremely modest results, reported sales surpassing all expectations.

According to experts, the major producers, De Beers and ALROSA raked in totally about $ 2 billion in rough sales during the first quarter. De Beers posted sales reaching $ 1.15 billion – almost $ 610 million in January and $ 545 million in February. Unlike De Beers, ALROSA holds trading sessions every month, but these are slightly leaner in volume. According to estimates provided by market sources, the Russian company sold $ 1.2-1.4 billion worth of rough goods in the first 3 months of 2016, carrying out approximately equal monthly sales.

The both companies posted sales, which were higher compared with one year ago – despite the fact that they adhered to a conservative pricing policy. ALROSA keeps prices unchanged since September 2015, when it reduced them by 8%. De Beers cut prices by 8-10% in February, bringing them in line with market expectations.

This conservative policy gave results. Data coming from trading platforms suggests that the average world price of diamonds not only stabilized, but also began growing. Since this growth was not underpinned by miners, it means that it is due to business activity in the secondary market and high demand at tenders. Market players say that, for example, rough diamonds sold at the recent tenders held by Petra and Rio Tinto were traded at premiums, sometimes reaching double digits.

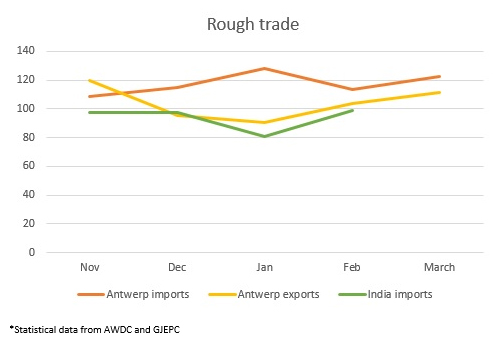

The average price of diamonds imported to and exported from Antwerp points to an overall trend towards growth versus the end of 2015. In March, the average price of diamond imports to Antwerp was $ 122 per carat, while that of diamond exports – $ 111 per carat (the difference was due to the fact that some part of expensive rough remains in Antwerp for cutting). This is lower than in March 2015, but significantly higher than in the previous month. Diamond import prices registered in India show a similar trend.

Waiting period

At the same time, trade volumes declined in March both by value and volume compared with February. Both rough imports to and rough exports from Antwerp fell by an average of 20%. GJEPC has not yet published its data for March, but one can expect a comparable movement.

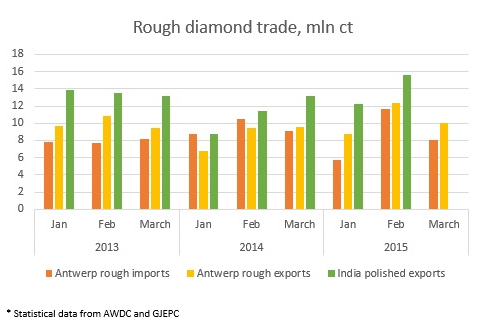

This slowdown, however, is not yet a reason for pessimistic forecasts. The diamond market has found a point of balance, and this assertion may be proved by at least two arguments. The first is about trade volumes. Although March sales were lower than February sales by volume, but they returned to the historical level of previous years, while they were significantly lower during the entire second half of last year.

Rising prices for diamonds may be taken as the second evidence. If the secondary market and tenders are clearing the way for premiums to diamond deals, it means that prices offered by rough producers are now on a fair level, giving the midstream an opportunity to earn more. And it is the low margin in the midstream, which is one of the factors breeding instability in the diamond pipeline.

Market players believe that the slowdown in business activities is due to completed restocking by diamond manufacturers. “By the beginning of the year, there was some shortage of polished goods, especially in the fast-moving categories of 0.5-1 carats, so diamantaires were busily buying rough diamonds to replenish their inventories,” one of them says. “However, starting from the second quarter the market will see coming polished goods made from rough purchased in January. So, the market takes a break – you need to see if polished prices will begin to decline after new batches of polished diamonds will be offered for sale.” According to RapNet, polished prices in March remained stable reflecting zero growth. April results will largely determine further developments.

In these circumstances, the best tactic for diamond mining companies would be to maintain sales at the current level for some time. Currently, rough sales are in sync with their historical levels and the market is unlikely to digest more. Further price cuts will devalue the inventories held by diamond manufacturers and accumulated in the first quarter. On the other hand, pushing prices up will once again deprive diamond cutters of their margins and opportunities to increase business activity.

In this regard, the report by Bloomberg that De Beers raised prices by 2% looks very disturbing. So far, there was no confirmation of this, however, and one of the sightholders, Smolensk-based Kristall even denied it, saying there was no changes in prices in the assortment of rough it bought from De Beers.

ALROSA will kick off a regular trading session for its long-term customers starting from April 12, 2016 and until now there is no information if the company plans to change its prices or offered amounts of rough. However, speaking at a conference for investors in late March, the president of ALROSA said that “it was expected that the market would be stable and would not be subjected to corrections until the end of the year.”