Profit is the new turnover in the diamond trade. As retail inventory levels continue to shrink due to recession-driven efficiencies, the trade has had to change its mindset. No longer can diamantaires play the high-volume production game: they have to do more with less.

It seems 2015 provided the wake-up call which enabled a more profitable trade this year. Some credit, though not all, can be given to the mining companies who carefully limited supply this year.

[two_third]

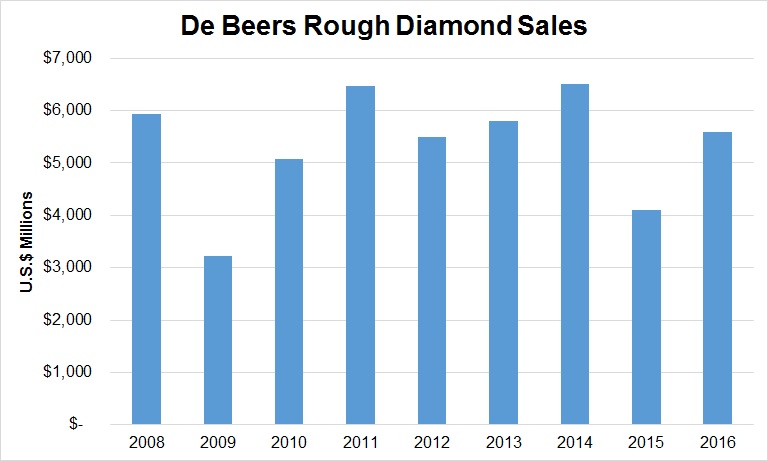

Still, with the final sight of the year now over, De Beers sales rose an impressive 36 percent to about $5.83 billion in 2016. While in the past that would have triggered the uncomfortable sense the “syndicate” is profiting at the expense of the trade, this year feels a little different.

The disproportionate correlation between rough diamond prices and their polished counterparts was less extreme than in previous years, even as it still exists.

[/two_third][one_third_last]

“Things changed in the last 18 months as manufacturers refused to buy overpriced rough in the second half of last year and mining profits slumped as a result.”

[/one_third_last]

De Beers rough index fell 5 percent in 2016 following a 15 percent correction last year. Meanwhile, polished prices, as measured by the RapNet Diamond Index (RAPI™) for 1-carat diamonds, dropped 2.8 percent in the 11 months to November, after firming 5.8 percent in 2015.