While the pandemic brought about an unprecedented shock to the whole diamond value chain in 2020, in a way it may also have acted as a catharsis of sorts for an industry that has been struggling to regain footing in recent years, in part due to a misalignment of supply and demand.

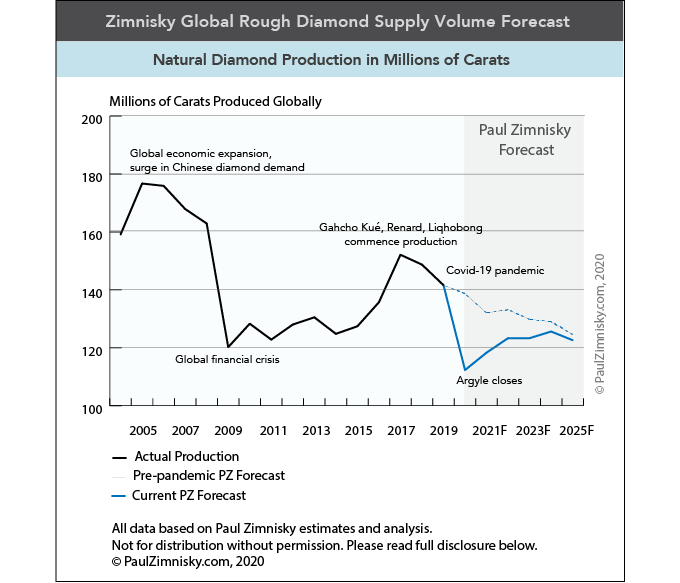

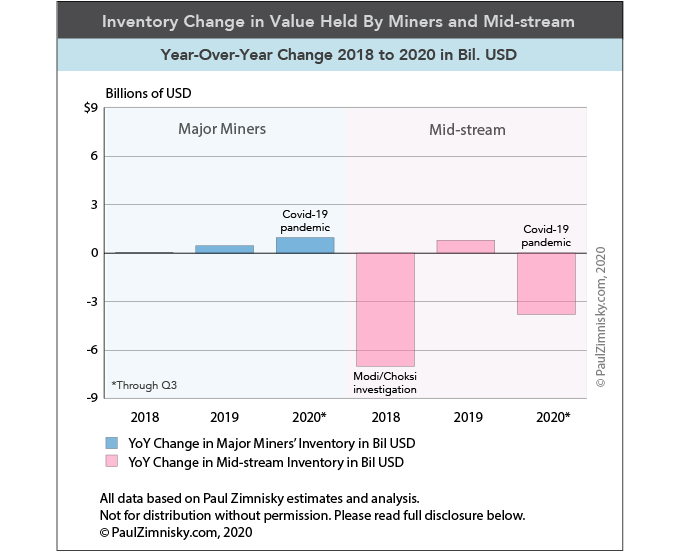

End-consumer diamond demand has been somewhat volatile in recent years, but for the most part it has been relatively resilient. However, on the supply side, a trend of increasing output has been apparent since rough diamond prices hit an all-time high in 2011. Excess diamond supply held by both the miners and the mid-stream, i.e. the manufacturers, has in part limited diamond price appreciation for most of the decade and thus has limited profitability for many industry players. For instance, a global basket of publicly traded diamond miners weighed by modified market cap in U.S. dollars, is down in excess of 60% over the last five years.

That said, challenging economics for the diamond mining industry has noticeably reduced exploration activity and new mine development over this time, which will undoubtedly limit new supply in the years ahead. Similarly, diamond and jewelry manufacturers, many of which have experienced apathetic business economics in recent years have transitioned to less levered and more efficient business models or exited the industry all together.

This shift in trend of lower mine output and more conservative business practices by the mid-stream has been accelerated by the pandemic. Multiple mines in the world’s most prominent diamond mining jurisdictions suspended production in 2020 due to government mandated lockdowns and also due to the subsequent market impact on business conditions. For context, six large-scale commercial mines globally have yet to recommence production following operation suspensions in March, April and May related to the pandemic. Consequently, global natural diamond production volume is forecasted to decrease by a significant 20% year-over-year to what is estimated to be the lowest output since the 1990’s (see above image).

Photo © ALROSA, Graphics © Paul Zimnisky .