De Beers’ Diamond Insight Report, released this week, is built around one of its favorite topics: The long-term supply-demand outlook for the industry. “Industry fundamentals support long-term confidence in sector,” trumpeted its release.

The thinking goes like this: Supply will be limited in years ahead, as no major new mines have been found, and the bigger productions are slowly but surely losing steam. However, demand is set to grow exponentially in emerging markets such as India and China. Therefore, demand will outstrip supply, and prices will rise.

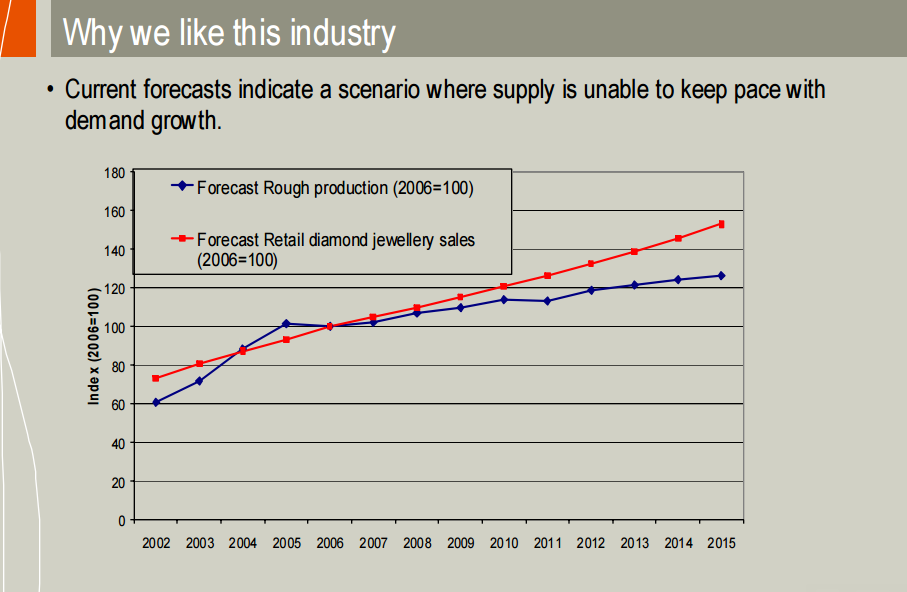

These fundamentals have been the subject of numerous charts, which show up in just about every diamond-industry presentation. For years, I used one in my presentations, created by since-departed miner BHP. I called it “the diamond industry’s favorite chart”.

One year, when putting my PowerPoint together, I realized the numbers were out of whack. We did not see a big supply-demand gap beginning in 2008. A few months back, Bloomberg noticed this too and reprinted a group of charts showing perpetually moving goalposts. “[The] long promised diamond supply gap stubbornly refuses to materialize,” wrote reporter Thomas Biesheuvel.

What went wrong? The supply situation has, it’s true, been mostly steady (though recycled diamonds and synthetics might be under-the-radar factors on the supply side). Demand, however, has seesawed unexpectedly.

In 2008, after a heated summer of speculation, the global financial crisis killed the economy throughout the world, and prices sank. A few years later, India and China started fulfilling their much-talked-about potential, and diamond sales posted double-digit gains in both markets. In 2010, it looked like the big pull away had finally come: De Beers’ diamond prices jumped 27 percent that year. “I have been in the business for 20 years, and I have never seen such dramatic increases,” one dealer told me then. The increases continued the next year—so much so that a commercial labeled diamonds 2011’s “best investment.”

But as the economies in China and India cooled, so did the diamond business. Now here we are, in 2015, facing a supply glut rather than a shortage.