It was an unusual year indeed for the rough diamond sector of the diamond pipeline. Prices were hiked and decreased, The DTC moved to Botswana, Alrosa made the long-awaited public issuance, tenders took hold and banks, for the first time, took a public stance against the wild chase after rough and their subsequent rising prices.

As always, De Beers’ last Sight of the year was a relatively smaller one, estimated at $550 million. In the secondary market, premiums were back, and once again, trade in DTC boxes became a way to generate some revenue.

The goods, while still priced high from a manufacturing perspective, were in many cases unchanged in practical terms – the list price of many boxes was higher but the composition of those boxes included more goods of larger size, which pushes up the price.

2013 – Mixed demand

For the year, the perspective is more complex. Manufacturers said they had no profitability, yet reported that 2013 was an improvement over 2012. The uncertain global economic outlook led to hesitant diamond jewelry purchases with retailers insisting on keeping price points under control, this echoed up through the diamond pipeline, forcing manufacturers to lose margins. The response – a demand that miners lower prices.

That is a known story by now, and becoming a ritual of sorts. According to one insider: “At the start of the year the prices [of rough] are reasonable, and then [miners] start raising prices until polished becomes uneconomical,” he said. “Buyers start refusing goods in the summer and then towards the end of the year, prices soften.” In broad strokes, this is a very accurate description of the rough sector in the past year.

During 2013, a number of items became more popular, Specials (+10.8 carats), for example. Goods weighing 5-10 carats were stable. The improved demand for VS2-SI2 polished goods affected the price of 5-carat and smaller rough that generates these goods.

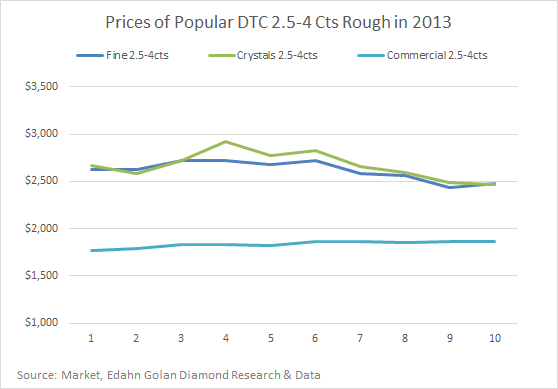

After the Hong Kong trade fair in September, demand for 2.5-4 carat rough decreased, as demand for smaller goods in polished waned.

Overall, during the year, prices of larger commercial goods steadily increased, in response to good demand in the polished sector for commercial items. Conversely, the Fine and Crystal boxes, where prices were hiked at Sight 3 and 4, met with resistance in the market. The 2.5-4 carat goods were steadily brought down throughout the rest of the year.

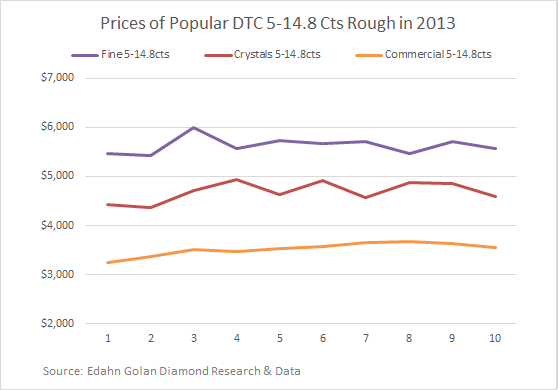

De Beers tried to keep up the price of the bigger goods, 5-14.8 carats, yet at the end of the year they were priced lower: In January 2013, the price of the Fine box was $5,456 per carat, by Sight 3 in March up to $5,995 p/c, and in December down to $5,563 p/c.

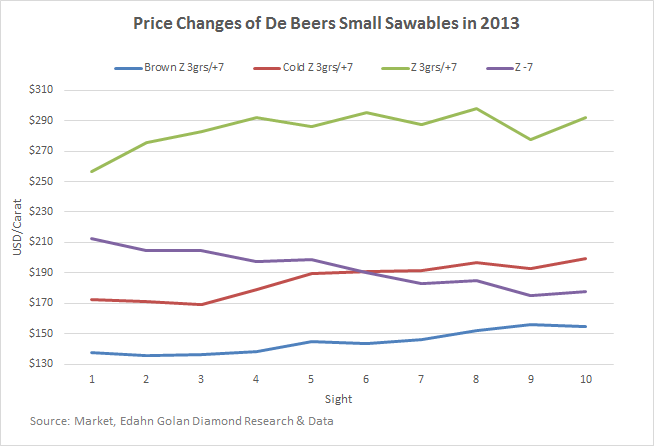

Among the cheaper smaller goods, the action was mixed. The -7 Sawable goods were steadily losing interest, while most of the rest of the small sawable goods saw prices rising. In some ways, this is symbolic. The bigger, nicer goods were in decreased demand as the consumer market turned to cheaper smaller goods. Hardly the ideal for the diamond market, although it is nice that the more abundant goods have consumers interested in them.

Is rough completely out of sync with polished?

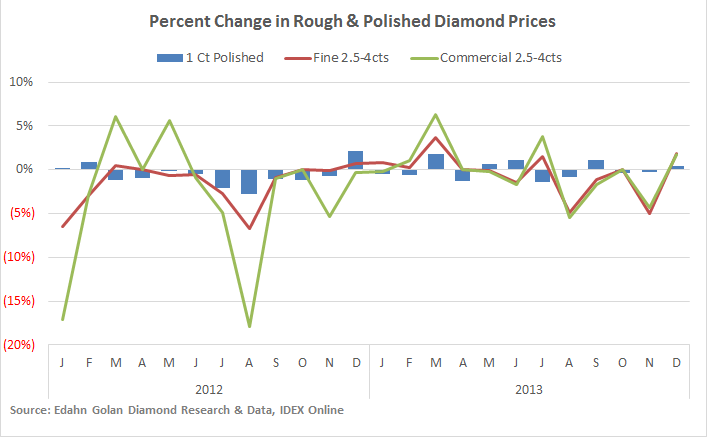

As recently shown in the January 2 Memo column “The Year Prices Were Polished Down,” prices of rough goods were not completely out of sync with polished. In the column, price changes of the most popular diamond item, 1-carat rounds, were compared to those goods from which they are polished – 2.5-4 carat rough. Specifically, the prices of the Fine and Commercial goods in these sizes. They were selected because of their popularity.

As the graph below shows, De Beers responded to the polished and manufacturing market, lowering and raising prices of their boxes in accordance with changes to prices of 1-carat rounds. For that, the usually bashed-by-the-press De Beers, specifically DTC, deserve recognition.

As the graph demonstrates, fluctuations in rough prices are far wider than those of polished. In the secondary market, the price fluctuations of rough diamonds are even wider because of premiums. These fluctuations moderate as the diamonds move down through the diamond pipeline, tapering off at very little change by the time they are offered in stores.

This explains the point made above about retail price resistance. The large retailers offer price points and plan their offerings in advance. Retailers know how to sell to consumers, and are a lot less interested in negotiating frequent changes in prices. In their perfect world, prices are motionless.

Tenders

Tenders, once the scrooge of diamond supply, have become an established source of supply in 2013. “People got used to it, they live by its rhythm,” said a veteran rough trader who added that many companies developed a specialty in attending and winning goods at tenders. “There are manufacturers that are ‘strong’ at this system, learned to handle them. More people view tenders as a good way to be supplied,” the trader added. “This is a change in perception.”

Tenders, many of them held in Botswana. Antwerp and South Africa are the preferred sales method of mid-sized and smaller miners, however De Beers, with Diamdel, and Alrosa are not shying away from it.

However, the tenders that got the most attention were not held by a diamond miner, but by a government. Okavango, a Botswana owned diamond seller is supplied by De Beers as part of a deal to transfer more of the income generated by the country’s main resource into the country’s hands.

The first tender concluded with very high prices, according to participating traders. The following tenders ended with lower prices and the last tender was cancelled. Apparently, the company decided to not offer any goods in December. This raises a question: if the idea of establishing a company like Okavango is to generate regular business, why halt business when the situation is not convenient? In an ideal world, that is not a bad idea, but in this flawed one, clients want stability, knowledge of what will become available and when. Food for thought.

Outlook

If the financial market is a good indication, despite the many concerns, during 2013 the global economy improved. Both the S&P 500 and NASDAQ soared, while gold dropped, in other words, investors moved away from the safe haven they run to when the economic situation is not well, towards the riskier stock market. That is a sign of confidence in the economy.

Not all stock exchanges boomed in 2013, however, so the road ahead is still bumpy, but there is no point seeking certainty. However, if it was all pinned on the global economy, demand for diamond jewelry will grow in 2014 – and by extension, so will demand for rough.

The problem is that consumers are not as dead-set on diamonds as they used to be. To grow demand, more than just a decent economic climate is needed. Strong and successful marketing efforts are essential, as are educational programs that would raise consumer awareness of natural diamonds, the role grading labs play and value of a high quality diamond. The industry cannot simply count on competitive price points and the occasional headline grabbing record prices achieved at auctions.