After having been almost scrapped in 2007, De Beers’ secondary market seller Diamdel underwent profound renovation when the company decided to transform it in an online auction sale program.

Since then, Diamdel has become an important source of income, totaling US$405 million in 2011, according to official De Beers statistics. Even during the ongoing economic recession Diamdel keeps expanding: new offices were opened in Dubai and Hong Kong, chasing the emerging Eastern markets that have not been depressed by the crisis. While Diamdel’s online sale system brought a wind of innovation in the rough diamond market, it also threatened to destabilize a well-oiled mechanism based on a selection of trusted buyer, the Supplier of Choice program.

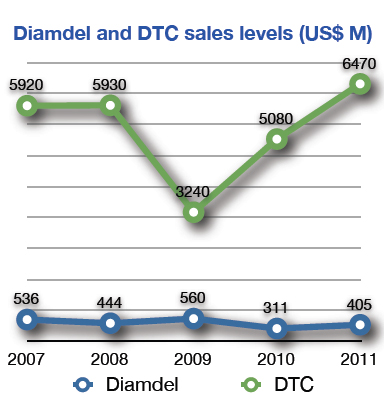

DTC and Diamdel: Two opposite approaches

The idea that diamonds are an exclusive luxury product that should be traded only through a small elite of reliable partners has been a linchpin of De Beers’ philosophy for years. When the other heavyweight in the rough diamond business, Russian company Alrosa, took field in the early Nineties, its management followed the same principle. As a result, most of the market is based on solid and trusted suppliers. Reliability and trust add value to the diamond product and buyers at all levels are happy to spend more for this insurance. Diamonds are luxury goods, and an exclusive and impeccable supply chain adds value to the product.

When the new Diamdel was presented, two major concerns arose from diamond operators. The first one was that De Beers would have slowly decided to renounce to the Supplier of Choice in favor of the more remunerative Diamdel system. A wholly auction-based system would fragment the diamond supply chain; buyers intentioned to put a De Beers diamond in their pieces of jewelry would have to chase dozens of ever changing small buyers (whose credibility would be hard to verify), instead of simply contacting one or more designated sightholders. The second concern was that Diamdel could have prompted producers to set their own online auction systems for rough diamonds. As online auctions involve scarce social interaction and are easy to replicate, diamond producing countries could decide that they do not need to rely on the De Beers supply chain anymore, as it would be more convenient for them to sell rough diamonds directly. In this case, we should expect the iconic stability in rough diamond price compared to other products (such as gold) to vanish, shattered by the volatility that a great number of online auctions competing one with the other would cause. Volatility would also infuse fear in diamond investors, and their panicked reaction could have disastrous consequences for the market, that could be flooded by their stocks.

If in quiet times Diamdel’s online auctions created concern, the global recession added fuel to the fire. In the beginning, Diamdel did not interfere with DTC selling operations, as bidding prices during auctions were constantly above the ones proposed to sightholders; Diamdel was either used by sightholders who wanted to increase their stocks or by other buyers chasing better prices or trying to prove their credibility as potential DTC sightholders. Over the last few months, though, the spread between rough and polished diamonds has sharply decreased. Normally this would produce a decrease in rough diamond prices, but the DTC refused to make anything but small price adjustments. As a result, many Sightholders were forced to decline purchases, at risk of losing, in the long term, their beneficial status. The reason for the DTC not lowering rough prices to match the actual demand is an attempt to push polished prices up again, even at cost of not selling some diamond boxes in the short term. The message is clear: DTC intends to treat diamonds as luxury goods, protecting their price in tough times.

Unfortunately Diamdel did not seem to receive the message. In recent auctions selling prices were allowed to plummet down to 10% below the red line of DTC levels; even after price adjustments were made by the DTC in September, Diamdel made some small sales below its level. Buyers were so outraged that De Beers Managing Director Philippe Mellier had to call Tacy analyst Chaim Even-Zohar to reassure him (and, more importantly, reassure buyers) that Diamdel will not be allowed to accept bids under DTC prices anymore.

Putting things in perspective.

While concerns are legitimate when new selling systems are added to an oiled and trusted one, it is necessary to put things in the right perspective. The success that Diamdel auctions experienced in the last few years is mainly due to its small size. De Beers is obviously keen to stress that Diamdel has made one sold out after the other, but if we consider that its sales volume has been cruising at around one tenth of the DTC for years, this should not be surprising. De Beers is simply underexploiting the potential of its auctioning mechanism, and if it does so it means that its management still believes in the Suppliers of Choice program as the predominant selling system. It should not come to a surprise that an auction presenting a large number of bidders (sightholders and non-sightholders), buying a relatively small stock of diamonds at competitive prices would produce a sold-out effect. But since the birth of online auctioning never has Diamdel’s volume threatened DTC’s supremacy, nor there is a long term trend suggesting that it will in the future (as shown in the comparative figure on the left).

The impact of Diamdel on the market should therefore neither be under nor overestimated. At the present time auctions represent a potential valve for a diamond market shattered by the excessive cost of rough diamonds compared to polished ones. By using Diamdel, De Beers ensures that, whatever the outcome of sights, a certain amount of roughs will enter the market via auctions and, as long as they do not saturate the auction system, the exclusivity of the De Beers brand remains intact. In the meanwhile, De Beers can use Diamdel to get a real-time pulse of the rough market: in this fluid period characterized by a profound crisis in the traditional markets and the rising of East Asian markets, it is important for De Beers to individuate new strong partners who could, in the future, apply for sightholder positions. On the other hand, the Supplier of Choice system has proved to be structurally more stable than online auctions and scrapping, or even weakening it further, could represent a risk too great to take for De Beers.

Concerns are understandable, as online auctions could be a real breakthrough in the diamond market. Nonetheless, if we look at the long-term picture, it appears that De Beers is, at the present time, keeping the dog at bay.