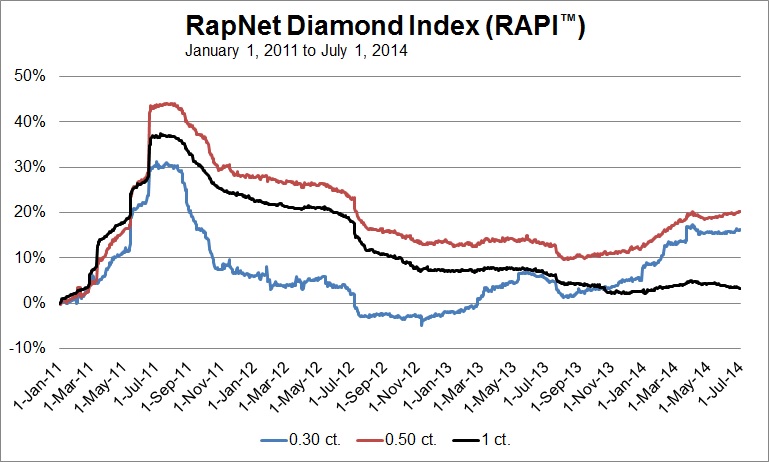

The second quarter was always going to be a quieter period for the diamond trade. Therefore, few were surprised that the RapNet Diamond Index (RAPI™) for 1-carat diamonds softened during the period, as reflected in the Rapaport Monthly Report – July 2014. This time of year is traditionally a slower period for the market, despite the fairly busy trade show schedule.

[two_third]

In the coming months, things will likely get worse before they get better. The third quarter tends to bring sharper declines before demand typically improves closer to the holiday season, when prices subsequently firm up. There is a cyclical nature to the diamond trading calendar that partly explains the current slowdown, and the almost positive mood that lingers is a reflection of the true strength of the first quarter that preceded the quiet.

The first quarter saw the strongest quarterly growth since the second quarter of 2011. Prices rose and demand increased during the first three months of the year due to inventory replenishment following the Christmas and Chinese New Year seasons. In fact, the increases were far healthier and more sustainable than three years ago, which has encouraged the skeptics.

[/two_third][one_third_last]

“The almost positive mood that lingers is a reflection of the true strength of the first quarter.”

[/one_third_last]

Back in 2011, the sharp price growth experienced in the first half of the year was largely driven by market speculation. Conversely in 2014, first quarter growth reflected steady demand filtering in from the retail sector. The U.S. Christmas shopping season was fairly robust and the Chinese New Year signaled that the market in China is still growing, even if it’s doing so at a slower pace.

[two_third]The diamond market has been cautious since 2011, having learned its lesson from the speculative bubble that ultimately burst back then. Today, diamond wholesalers and manufacturers are managing their inventory in a far more efficient and leaner manner. This was evident in the second quarter of 2014 when they scaled back their buying and avoided pushing prices higher in the market when it was not warranted.[/two_third][one_third_last][/one_third_last]

“2014 has been a relatively good year so far in terms of turnover. It has been less so, however, when measuring profitability.”

RAPI is based on the average asking price in hundred $/ct. for the top 25 quality round diamonds (D-H, IF-VS2, RapSpec-2 and better) with GIA grading reports offered for sale on RapNet – Rapaport Diamond Trading Network.