ALROSA has published an update of its reserves and resources estimated under the JORC Code. These figures once again confirmed the company’s claim for leadership in the global diamond market.

One and a half year passed since the last assessment of ALROSA’s resource base under JORC. Judging by the figures published on the miner’s website its rough diamond reserves fell by 3.7% (or by 23 million carats) and reached 607.5 million carats as of July 1, 2013.

What can be said about this figure? At the very least, the company is more or less successfully makes up for the amounts of rough being extracted: ALROSA produced 51.5 million carats of diamonds during this period.

ALROSA explains the decline in reserves due to recalculation of reserves available at the Udachny Underground Mine, which eventually decreased by almost 22 million carats. At the same time, the Aikhal Mine increased its reserves by 9 million carats, while the deep level reserves of the Nyurbinskaya Diamond Pipe went up by 15 million carats.

As a result, the total resource base possessed by ALROSA has slightly increased in comparison with the figures for January 2012 and reached 973 million carats.

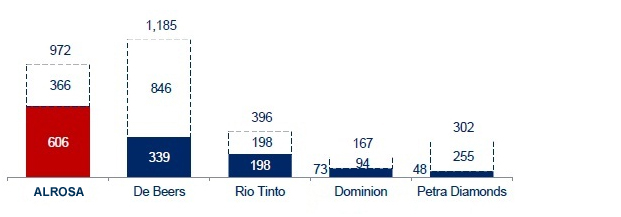

Here is how it looks in comparison with other major diamond mining companies*. The painted area shows the amount of reserves, while the total number (within the boundaries delineated by dotted lines) denominates the total resource base, including resources.

* Source – JORC-compliant data from ALROSA and statements from the mentioned companies

This diagram is not absolutely correct, because the data on stockpiles held by other companies do not reflect data on July 1, 2013, but as a rule for 2012. However, the diagram reflects the general trend.

De Beers is setting pace in terms of its total resource base, but ALROSA is a clear leader in terms of its reserves – that is from the point of view of its rough stockpile, which is well explored and guaranteed to be economically feasible for mining.

If we assume that in the future the two companies will maintain their production at the current levels (34 and 28 million carats per year, respectively), then the reserves held by ALROSA will last for the next 18 years, while those of De Beers for 12 years.

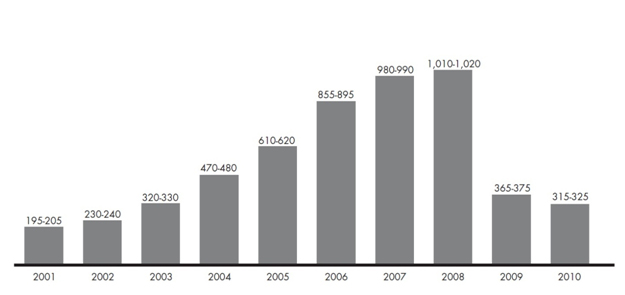

Of course, the possession of a resource base contains an element of luck. The fate decreed to place a number of diamond deposits in one area in Yakutia. But there is another factor, which is the cost of exploration.

According to the Bain report on the global diamond market in 2011, exploration works significantly diminished across the world in recent years.

Global spending on exploration ($ million) *

*Bain’s report for 2011

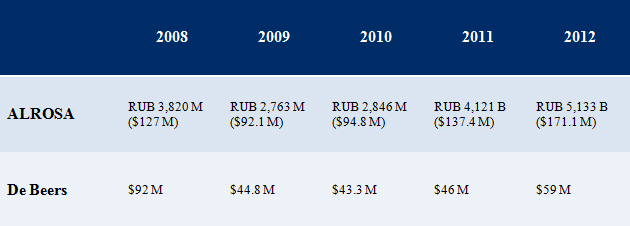

That said, if we compare the data on financing exploration over the past 5 years, it will turn out that ALROSA spent significantly more than De Beers on exploration.

Exploration costs (according to statements released by the companies, with the exchange rate being 30 rubles per $ 1):

The discovery of a diamond deposit and evaluation of its reserves and resources takes several years, while a further launch of mining operations may take away another 10 years. The data on exploration financing suggest that in the future ALROSA will only increase its breakaway from De Beers in terms of reserves due to more intensive exploration.