I’ll open with a confession: I don’t know where I’m going with this text. I usually start writing knowing what I want to say, and with a conclusion in mind. The conclusion is a destination. But not today. The thing is that it’s not just me – it’s the industry too. We don’t know where we are going, and that is the set up for a bankruptcy, a very disturbing thought.

It has yet to be published, but a major diamond company is apparently going down. The size of its debts are unknown at this point, but the scale is understood – in the many tens of millions of dollars. The debts are said to be split about half and half between banks and the diamond industry.

The company is considered a well-established one, not known as a risk taker or as a company that pays exuberantly for its rough, and to me this is the most disconcerting aspect. A company that at least appeared to act prudently has taken a major hit. Not a reckless company, not one that gambled big on odd ventures, not a company that relied heavily on supplying goods on memo to American specialty retailers. None of these to my knowledge. Nobody ever spoke negatively about them. Just a “regular” company.

The fallout I

Traders in the market in which this company is based say they are already feeling the fallout: people are nervous, morale is plummeting, trust levels are low, and companies are being cautious in their dealings with other companies. The outcome is that payment terms on new transactions are shorter, liquidity in the market is an issue, and many are operating under the assumption that matters in that center will further deteriorate, as all are waiting to see just who will be affected.

In other diamond centers, traders are starting to express concerns too. One called the news “a disaster” for the market.

The first concern is who will be hurt. If your suppliers hear that you are a creditor that may not get paid, they worry about you, view doing business with you as a risk, and act accordingly. They may charge more for the goods or trade only on a cash basis. That hurts an indebted company even further, exacerbating the situation. The bigger the fall, the larger the fallout.

So what set up the latest bankruptcy?

For some time, issues have been brewing in the market. For starters, polished diamond prices are continuously sliding downwards, as the Mercury Diamond, IDEX, and Rapaport indexes show.

Mercury’s MDGT is down for the 32nd consecutive month; at 118.96, the IDEX polished price index is at its lowest point since December 2010; and Rapaport states that prices of 1-carat rounds are down 7.1% year-over-year. The picture is clear.

Next, the level of demand from the consumer market is softening as well, which explains the decrease in prices. In turn, polished diamond inventories held by the mid-stream of the diamond pipeline are also an issue. According to data from Mercury Diamond (a client of mine), the volume of inventory of triple X, non fluorescent rounds has more than doubled since January 2016.

Based on my own tracking of the market of round-shaped diamonds, I see an increase of more than 37% in the quantity of diamonds held by the midstream compared to July 2016. Roughly speaking, this is a rise of a third in the amount of manufacturers’ capital that is tied to inventory.

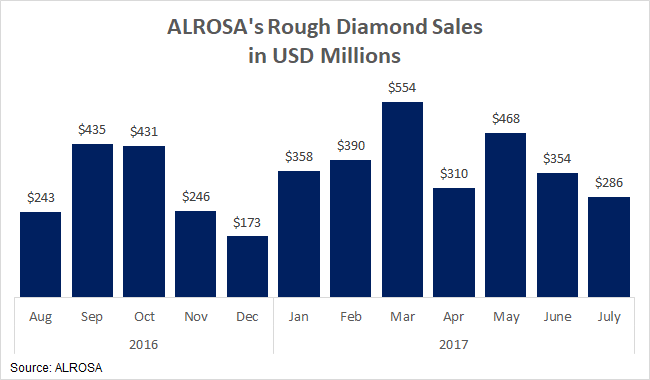

While polished diamond prices are declining and inventories are rising, rough diamond supply is plowing ahead. ALROSA increased production during the first half of 2017, and the volume of sales rose, totaling $2.44 billion.