Nothing should have surprised the diamond sector about KBC’s announcement that it is closing down the operations of the Antwerp Diamond Bank (ADB). It was not just the many rumors in the Antwerp and global markets in the week before the announcement or the news report about it in a local daily that should have prepared us for the statement. Ever since the October 2008 financial crash, it has become clear that the global banks view the financing of the diamond trade as less than attractive. A departure was not only on the books, it flashed in blazing, diamond-sparkling, lights across the sky. So why was the industry shocked? Probably because of the implications for the trade and what the announcement says about it.

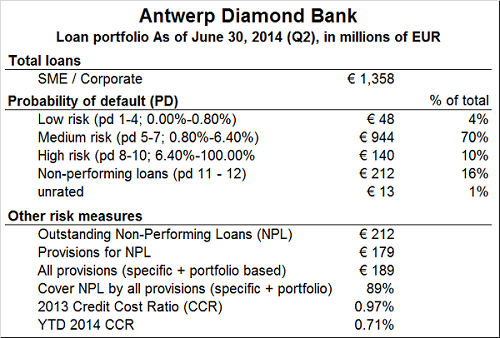

According to ADB’s parent company, at the end of the second quarter, on June 30, ADB had €1.358 billion in outstanding loans, or about $1.85 billion. This is a surprising figure. In December 2013, when KBC announced the deal to sell ADB to the Yinren Group, KBC disclosed that ADB has a loan portfolio of €1.2 billion. This indicates that over a period of six months, ADB may have increased the credit it extended to the diamond sector by 13%.

The rise in extended credit is interesting because it does not represent the general trend: Banks are decreasing their involvement with the diamond industry, or leaving it altogether.

Bad news: 12% of global diamond financing is leaving

KBC’s decision not only puts an end to the hope that Yinren will give ADB a new lease of life, but that nearly $1.9 billion in bank financing will slowly shrink to nothing. Diamond industry bankers estimate the global diamond industry’s financing at about $15 billion-$16 billion, which means that some 12% of it will be called back in, repaid and not come back, at least not in the near future.

The $15 billion-$16 billion figure is spread across the entire pipeline from mining and exploration efforts, through polishing, to wholesaling and at least part of diamond jewelry manufacturing. However, ADB finances the most sensitive part of the pipeline – rough buying, manufacturing and polished wholesaling – that relies heavily on ADB. The most sensitive part of the industry is suffering the blow.

Why is it happening?

The diamond industry is transactional-based, and recuperation is slow with debts difficult to collect, ADB CEO and Executive Committee Chairman Pierre De Bosscher told me about a year ago when I was researching diamond-related bank financing. He and other bank managers raised similar points, which altogether tell the story of shrinking financing.

[two_third]Contrary to the diamond industry’s desire to see an increase in financing, the banks want to decrease credit levels. According to Erik Jens, CEO of ABN AMRO’s International Diamond & Jewelry Group, the leading provider of financing to the diamond industry, “There is too much financing, and not enough banks, but to bring in more banks, more transparency and more corporate culture and DNA is needed.”[/two_third][one_third_last]

“But to bring in more banks, more transparency and more corporate culture and DNA is needed.”

[/one_third_last]

De Bosscher said that financing goes to companies that best meet the following standards: consolidated financials, 25%-30% solvency, simple corporate structures and good corporate governance with higher transparency regarding movement of finance.

Instead, he and other bankers say diamond industry companies are over-leveraged, have complicated structures with companies in tax shelters, and have limited hard collateral. Because of that, in the eyes of banks, the diamond sector is considered higher-risk compared to other industries. So, naturally, given a choice, banks prefer lending money to other sectors.

Consider the following table. At the end of the second quarter, 70% of ADB’s loan portfolio was rated medium risk and 10% as high risk. Another 16% of the loans (by value) are rated Non-performing.

It’s not known why Yinren did not complete the purchase of ADB, or how much it agreed to pay for the bank. However, part of the deal included KBC keeping the more toxic loans – higher risk and non-performing loans with a net book value of €400 million – to sweeten the deal. The figures in the table above hint that €48 million in these loans have already been paid off.

The way from here: improved standards

With the withdrawal from the diamond industry of Bank Leumi in Israel and then in New York City while ABN AMRO was derisking and optimizing its loanbook and footprint, and now (unconfirmed) reports that Standard Charter Bank is also decreasing its supply of money to the diamond sector and now the winding down of ADB, the writing is clearly on the wall: The diamond sector must overhaul its financing in terms of transparency, corporate structure, but mostly with its own philosophy.

The ingrained instinct of keeping everything hidden and private does not work anymore. The light of day will cleanse the marginal issues that breed in the dark, but more importantly, restore the banking systems’ confidence in the diamond sector. As the heads of the banks have told the diamond industry time and time again, they need to see better corporate governance, better reporting standards (IFRS, for example) and a willingness on the part of diamond firms to play the game in a modern way, one that takes into account the banks’ ability to turn their backs to the industry – even if it’s a bank dedicated solely to the diamond sector.