Global production of rough diamonds in carats continues to decrease, as evidenced by the data of the Kimberley Process. Diamond output in 2011 reached 123.989 million carats, 3.4% down compared with 2010.

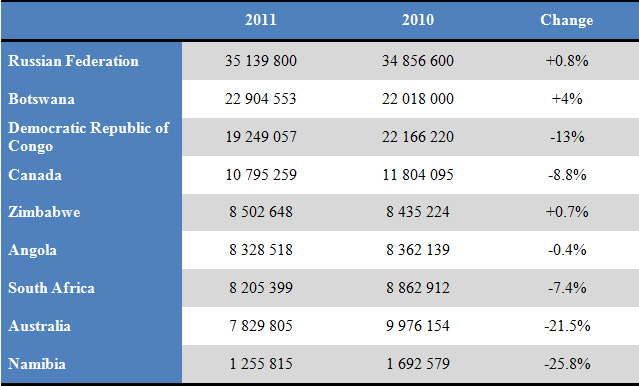

The overall picture of global production remained unchanged. Russia remains the leading producer of rough diamonds: in 2011, the country turned out 35.139 million carats (an increase of 0.8%). Botswana, ranked second, scaled up its production by 4% up to 22.904 million carats.

Based on the results of 2011, the top nine of diamond producing countries is as follows:

Other countries delivered hundreds of thousands of carats and are not comparable with the above nations in terms of their diamond output.

The statistics show that the downward trend in production is observed in most diamond mining areas, which is apparently explained in the first place by natural depletion of the existing fields.

Thus, Australia’s slump in production by more than 20 per cent is a direct consequence of the exhaustion of the Argyle Mine, which used to turn out about 40 million carats at its production peak in the 1990s.

It should be said that the downward trend in global diamond production will continue to develop not only due to the exhaustion of mine fields. Given the difficult market conditions, we can expect that diamond miners will cut production in line with the falling demand for rough. In particular, De Beers has already announced that it will reduce rough output this year. ALROSA has not yet announced any similar plans.

According to the Kimberley Process, the average value of rough extracted in 2011 reached $14.406 billion in the same year, which corresponds to an average price of $116.19 per carat.

Apparently, speaking about production cost the KP has in mind the so-called “producer book prices,” which primarily characterize the quality of stones and cost of production. Compared with 2010, the average cost of rough in 2011 increased by 30.9%.

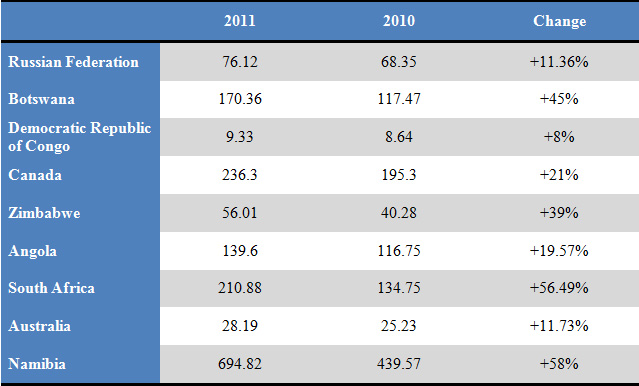

Russia, being the world leader in diamond production by carats is turning out rather cheap rough valued at $76.12 per carat in 2011 ($68.35 per carat in 2010). However, it should be kept in mind that about 35% of Russia’s output is the so-called industrial rough, which has a sufficiently low market value. ALROSA in its report for 2011 indicated that the average price of industrial diamonds was $7.7 per carat, while jewelry quality stones were valued at $196.9 per carat.

The highest prices for rough diamonds are found mainly in countries with low levels of diamond production. The most expensive rough in 2011 was mined in Lesotho – $1.602 per carat. Gem Diamonds, which is operating there, is specialized in producing rare stones having high quality characteristics. Traditionally, expensive rough is mined in Namibia – $694.82 per carat ($439.57 in 2010).

At the same time, diamonds from the DRC, which occupies the third place in terms of production in carats, are the cheapest – $9.33 per carat. The country produces almost exclusively small-size rough, making it invisible to the world market. Diamonds from Australia are priced at an average of $28.19, while the largest share in Australia’s goods is taken up by small-size rough from Argyle.

Prices for rough recovered in major diamond mining areas (USD):

At the same time, diamond transaction prices may differ from the book prices. For example, according to the KP, the average value of diamonds exported from Russia in 2011 amounted to $117.82 per carat.

According to the KP, in 2011 Zimbabwe exported its goods at a price of $54.31 per carat, though their book price was $56.01 per carat. This confirms the previously published reports citing some sources to the effect that because of an unclear legal status of diamonds coming from Zimbabwe this country sold them low to get at least some money for the rough produced.

India is still the largest final consumer of rough diamonds. According to the KP, the country imported 132.095 million carats of rough diamonds and exported 37.07 million carats in 2011. Thus, 95.025 million carats of diamonds were left in India for cutting purposes. In 2010, this number was 132.226 million carats. It can be assumed that the decline in purchases of rough for cutting was due to the liquidity crisis, which Indian diamantaires faced in the second half of 2011. The average import price of diamonds in India in 2011 grew by 59% – to $108.1 per carat.

The second largest diamond cutting center by the amount of rough consumed is China, where net imports of rough diamonds in 2011 totaled 6.095 million carats, having slightly increased in comparison with the previous year (5.46 million carats). The average import price of diamonds in China is $145.47 per carat, compared with $112.23 a year earlier.

Israel’s net imports of rough in 2011 exceeded the level of four million carats (4.042) for the first time since 2006. Prior to that, Israel used to retain about 2 million carats of rough every year.