Diamond industry conditions have recently been described as a “crisis.” In some segments of the industry anecdotes of “no business” have surfaced as well as “no demand” for certain categories of diamonds. A representative for a leading trade group of manufacturers in India has recently said the current “recession” is “worse than the one witnessed in 2008-2009” during the global financial crisis.

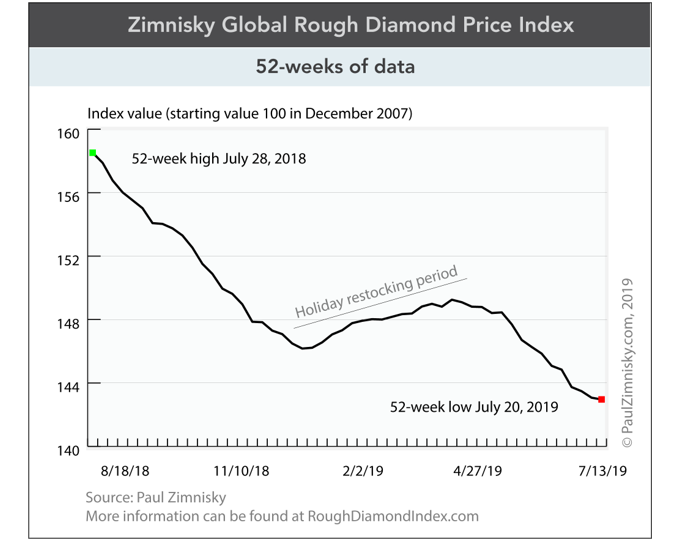

De Beers’ rough diamond sales in dollars are down 17% year-to-date through June compared to the same period last year. ALROSA’s (MICEX: ALRS) sales are down 33%. According to the Zimnisky Global Rough Diamond Price Index, a proxy for the like-for-like change of the global product mix, rough diamonds are down 2.3% year-to-date as of July 20 and are currently sitting at a 52-week low (figure 1).

Industry-wide challenges are understood and have been well publicized at this point: high inventory levels throughout the pipeline, a continued deleveraging of the mid-stream sector, reduced manufacturing credit availability, uncertainty surrounding the proliferation of man-made diamond jewelry and weak downstream sentiment related to macroeconomic and geopolitical factors.

On July 18, De Beers’ parent, Anglo American (LSE: AAL), cut 2019 diamond production guidance to approximately 31 million carats, down from a previous range of 31-33 million. However, even at the high-end of the previous range, De Beers production was expected to fall by over 8% year-over-year as supply is inevitably impacted by the closing of legacy mines: Victor, Voorspoed and Elizabeth Bay. In addition, the timing of the transition to underground mining at Venetia further curtails production capacity this year.