Larger diamonds with J grades and down are gaining popularity among wealthier US consumers. What’s driving the craze?

Large diamonds in low colors are a hot market in the US. The Rapaport Intelligence Report asks why.

The trend represents an important shift in how higher-end consumers perceive diamonds. Those seeking 2.50-carat and larger goods are increasingly asking for J grade or lower, and sometimes a long way down the color scale, jewelers and dealers report.

The main impetus, sellers say, is consumers’ preference to show off that their diamond is natural. Lab-grown diamonds overwhelmingly have high color and clarity. A D-flawless is no longer an obvious flex in an era in which, according to TheKnot, 61% of American couples are opting for synthetics when buying engagement rings.

The latest issue of the Rapaport Intelligence Report, formerly the Rapaport Research Report, investigates whether this development is visible in retail and wholesale data, including in exclusive Rapaport figures on pricing and trade flows. It also looks into who’s buying these diamonds, how celebrities such as Taylor Swift influenced the movement, why stones with these colors are especially strong in antique cuts, and how the topic relates to De Beers’ campaign promoting Desert diamonds.

The diamond industry has started to show signs of recovery in certain areas. Goods in 2-carat and larger sizes were already relatively solid, outperforming smaller stones over the past year, especially in long fancy shapes. This report pinpoints a specific area where jewelers have enjoyed growth and asks whether this segment is safe from the threat of lab-grown replacement.

In addition, this month’s Rapaport Diamond Price Analysis focuses on a sharp improvement in prices of 0.30-carat collection goods in April. We explain why this happened, zeroing in on individual categories that saw sharp upward corrections in the past month and a half.

As always, this report presents exclusive Rapaport data on 0.30-, 0.50-, 1- and 3-carat diamonds, including average prices, discounts, inventory by country, search volume, and turnover time.

The industry will gather in Las Vegas later this month for the JCK and Luxury shows, the most important indicators of the US market’s condition. The trends this report outlines are likely to be visible on the exhibition floors.

Why Low-Color Diamonds Are in Vogue

Lab-grown diamonds have transformed the jewelry business in ways that we have outlined in multiple editions of this report. One of the impacts that perhaps gets less attention is how synthetics have altered preferences for those who still want to buy a natural diamond.

One such example is a shift to low colors, the topic of this issue of the Rapaport Intelligence Report. US dealers and retailers report growing interest from relatively affluent consumers for diamonds of around 2.50 carats and larger in approximately J color and down in round shapes and, especially, in long fancies and antique cuts.

Sellers consistently cite the same reason: Shoppers want to make it very clear that their diamond is natural.

The Retail Data

The Clear Cut, an online natural-diamond retailer based in New York, saw a 115% increase in sales volume for K to O colors between 2023 and 2025, according to Olivia Landau, its cofounder and CEO. This coincided with the company’s highest average order values, at around $30,000 — indicating budget pressure was not the factor.

So far there is little market-wide data to support the trend, even though anecdotally high-end jewelers cite the shift.

Retail sales of 2-carat and larger natural diamonds in round, cushion, pear and old mine shapes with J to M color and VS or SI clarity rose 9% by units in 2025, according to data from Tenoris, a provider of diamond and jewelry analytics. Value increased 4%. The figures cover sales of loose stones and finished jewelry at US specialty jewelers, in all cases with grading reports from the Gemological Institute of America (GIA).

However, that is broadly in line with the wider market: Sales of diamonds with those same criteria but with D to L color rose 8% by volume and 6% by dollars in 2025, said Edahn Golan, comanaging partner of Tenoris.

Sales in the lower color range were flat by value and volume in the first quarter of 2026, with high colors down 1.5% by units and up 0.5% by value.

The Wholesale Facts

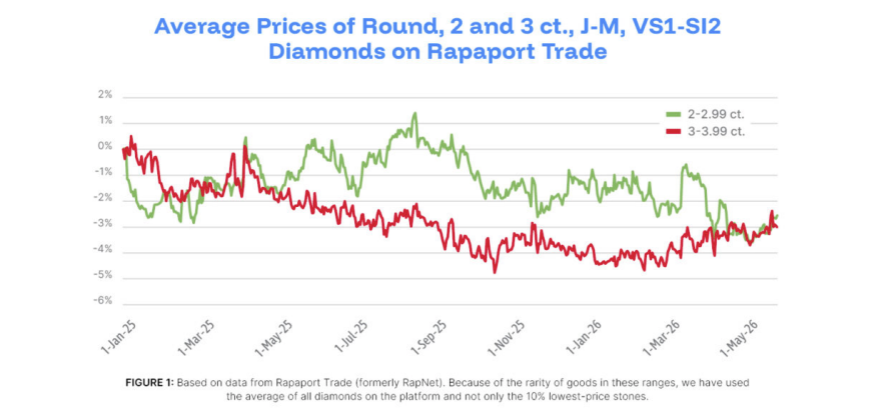

So far, the trend at wholesale is only visible in specific areas. Average asking prices for round, 3- to 3.99-carat, J to M, VS1 to SI2 diamonds on Rapaport Trade (formerly RapNet) increased 1.5% since the start of 2026 after declining throughout 2025.

Other categories did not show signs of a meaningful shift in prices.

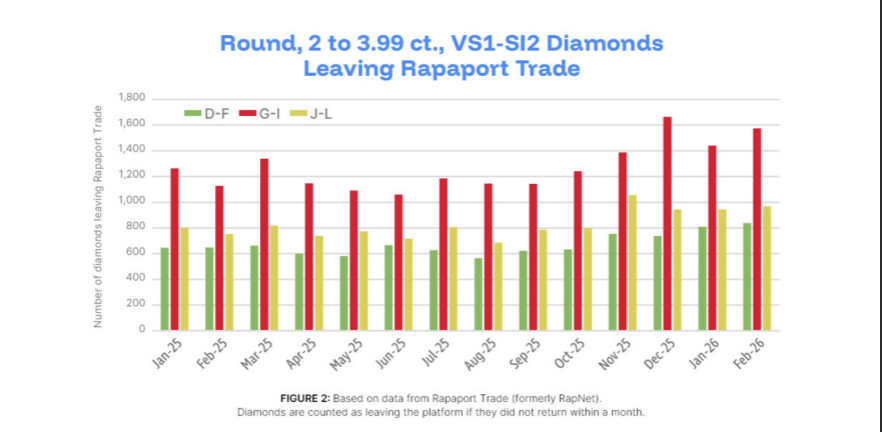

Data on diamonds leaving the platform — a rough indicator of sales — also show minimal signs of this development so far.

The overall number of diamonds leaving Rapaport Trade in round and oval, 2- to 3.99-carat, VS1 to SI2 goods with GIA reports progressed from late 2025 onward. This reflected overall strength in these sizes, mainly in the US. However, the growth appears to have been mainly in the mid-range colors (G to I), which are the more classic items for the American audience.

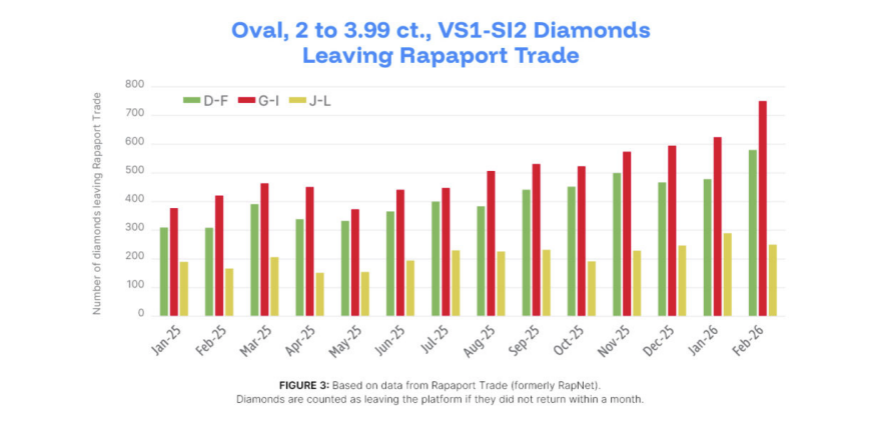

The exception is old mine cuts — a sweet spot for lower colors, albeit a relatively small market. The number of 2- to 3.99-carat diamonds in this shape with VS1 to SI2 clarity leaving Rapaport Trade increased gently throughout most of 2025 and spiked from October onward, perhaps because of Taylor Swift’s August 2025 engagement. J to L colors — which already have a larger share in old mines than in other shapes — accounted for much of the growth.

The Buyers

The American shoppers to which retailers and wholesalers refer are, by and large, not specifically looking for a bargain. They have budgets ranging from $10,000, maybe $20,000, up to $50,000. They could comfortably buy a 1-carat, D-flawless stone with perfect criteria. Instead, they choose a larger diamond with a warmer color. Many of these purchases are for engagement rings. Some are additions to jewelry collections for people who already own a more generic bridal piece.

Diamond synthesis and treatments have advanced to the level where most lab-grown stones on the market are D to F color. With 61% of US couples opting for lab-grown engagement rings — according to The Knot — consumers see more and more of their friends sporting large, high-quality stones that shine strongly from across the room but are decreasingly unique. This has pushed the more selective consumers to seek something different and more obviously natural.

The trend is part of a wider movement toward uniqueness — one that has also driven greater demand for fancy shapes and original designs. It’s also a trend that De Beers noticed a while back, prompting its Desert diamonds campaign, which initially focused on the more niche, brownish shades and is now putting more emphasis on colors slightly higher up the D to Z scale.

The Shades

This is a major change for the stateside market. It is well-known that American consumers have traditionally prioritized size in their diamond choices — a fact that helped synthetics sellers grab share by offering bigger stones for less. But another US tendency has been to focus on G to I colors — and F to H in fancy shapes — since these offer a compromise between quality and price. If the ring is in platinum or white gold, there is more incentive to get a higher-grade center stone, since the color shows up more than when placed in yellow gold.

Dealers that spoke to Rapaport break down consumer interest into four color ranges.

The first is D to I, the grades on which leading brands traditionally insist. Tiffany & Co., for instance, only accepts diamonds for its engagement rings down to I color, according to its website.

The next is J to L, which has become popular in those larger sizes, with consumers seeking a clearly natural stone that looks relatively colorless. M to around P is also getting traction, while Q to Z diamonds — which already look rather yellow or brown — have increasing popularity but are still niche.

Most of the demand for large, low-color diamonds is in rounds, longer cushions, oval, pears, old mines and European cuts, mainly in VS1 to SI2 clarity. While the International Gemological Institute (IGI) has a big business grading low colors, diamonds with GIA reports are more sought-after — a must for the higher-end consumers that are generally in the market for these goods.

The Celebrities

Celebrities have both reacted to and fueled the trend. The most famous example is singer-songwriter Taylor Swift.

Much has been said about Swift’s choice of an old mine cushion-cut and the resultant craze for that and similar shapes. Less has been said about the apparently low color she and fiancé Travis Kelce chose.

While media reports mostly quoted one estate jeweler as saying the diamond was around F color, several diamond experts who spoke to Rapaport estimated the real grade to be around J or L. This is a remarkable fact for a public figure who presumably had the budget for a D-flawless.

Other figures who opted for low-color diamonds include singer-songwriter Miley Cyrus and jewelry influencer Kira Kirby. Kirby showed off a yellowish, old mine-cut diamond to her Instagram followers last year.

The Antique Cuts

There is a strong overlap between low colors and antique cuts such as old mines, for which Swift and Kirby opted. Both features enable uniqueness and a rustic look, and they make a statement to the observer that the diamond is natural.

Of course, a diamond that is genuinely antique will be from the pre-synthetics era. While most antique shapes these days are newly cut by manufacturers trying to imitate the old style, this is generally not something that lab-grown consumers are buying.

Dealers say 2.50-carat and larger diamonds in low colors with antique cuts are a hot market right now.

In addition, GIA color grades tend to be more punitive for antique cuts than modern ones. The larger facets on shapes such as old mine and European cuts might reduce brilliance, but they make the off-white color less prominent. As a result, the stone faces up one or two color grades higher than what appears on the report. This gives consumers an opportunity for cost savings, though the general rarity of antique cuts offsets this somewhat.

“It is possible, especially with brilliant cuts such as the old mine cut, that someone might perceive the color differently [compared with the grade on the report],” said Al Gilbertson, senior research associate at the GIA and an expert in diamond cuts. “That is not uncommon when looking at a stone face up, outside the controlled conditions of GIA laboratories.”

Fluorescence is also less of a factor in low colors: The phenomenon can actually make a slightly yellowish diamond appear more colorless under ultra-violet (UV) light, according to a post on the GIA website. In high-color diamonds, some people perceive a hazy or oily appearance in fluorescent stones.

The Desert Diamonds

De Beers’ Desert diamonds campaign, which it launched at the 2025 JCK Las Vegas show, tapped into this trend. It aimed to promote natural diamonds in general by emphasizing the sandy colors that the earth produces.

The industry initially received the idea with a degree of confusion, since brown diamonds are very niche and relatively inexpensive. At the time, polished manufacturers believed this was an effort to shift inventory of low-color diamonds that De Beers had accumulated during the market downturn of the last three years.

Desert diamonds is just a “metaphor” for natural, De Beers later clarified. It’s not specifically trying to shift low-color goods, but rather using the varied, unique and authentic colors of natural diamonds to stimulate curiosity and entice consumers into retail locations. The campaign has driven 8.6 million people into stores, according to Sally Morrison, natural-diamond market lead at De Beers.

A three-stone ring from De Beers’ Desert diamonds bridal launch. (De Beers)

That said, De Beers’ recent addition of bridal jewelry to the Desert diamonds theme indicates the company is serious about promoting sales of the diamond colors that are in the ascendency. The bridal campaign, which it launched in April, promotes a “softer, lighter desert palette that testing indicates resonates strongly with bridal audiences seeking authenticity and individuality,” De Beers said.

While Desert diamond tones start at around K or L color and go through to dark browns, “for bridal, we focused on the very light end of that spectrum,” according to Morrison.

“It was very clear in focus groups when we were testing the idea against a bridal audience specifically, or a pre-bridal audience, that those lighter, creamy colors are just much more interesting to them. There are fewer people that want a strong brown in an engagement ring.”

The Risks

The trend is a positive development for the large-stone market, indicating that there are many consumers who still insist on a natural diamond. This is only a limited part of the diamond sector, but it is increasingly the most robust segment as the industry shifts toward value over volume.

Dealers who spoke to Rapaport are confident the rebound in low colors will last, eventually feeding through to the midstream more substantially. Their basis for this belief is that lab-grown producers are not interested in replicating these sizes, and consumers are not interested in buying them. Synthetics’ selling point is size, high color and high clarity for lower cost. The relative safety from synthetics replacement was also behind De Beers’ Desert concept.

However, there is a risk that the same phenomenon that saw many consumers move away from classic natural bridal categories toward lab-grown will also take place in large, low-color diamonds.

The lab-grown industry built itself on imitating natural, tapping into consumers’ aspirational desire to own a product that could plausibly be the real thing but at a lower cost. Producers might see that large, low-color natural diamonds are popular with wealthier consumers and try to enter the market themselves.

This should be relatively easy for them. While technology for growing high-color stones and treating low-color ones has improved, a lot of stones made using chemical vapor deposition (CVD) still come out of the chamber with an off-white or brownish tint. The key for the natural trade will be to tie its product tightly to the story behind it.

Rapaport Diamond Price Analysis

April: 0.30 ct. Rebounds in Higher Qualities

Prices of round, 0.30-carat diamonds in D to H color and internally flawless to VS2 clarity improved in April, as the first table on Page 9 of the full Rapaport Intelligence Report shows.

In internally flawless to VVS, prices rose 1.7% for D to F and 1.9% for G to H. VS qualities did better still, rising 2.9% for D to F and 2.8% for G to H.

Growth represents the difference between the average of the asking prices for the 10% lowest-priced diamonds on Rapaport Trade (formerly RapNet) as of April 1 compared with the average for the previous three months.

It includes diamonds with RapSpec A3 or higher, meaning, for example, “Excellent” cut, polished and symmetry, and no fluorescence.

Price rises were scarce in the other sizes and qualities that the Rapaport Intelligence Report tracks, with the notable exception of certain 3-carat categories.

While 3-carat stones have performed well for several months, the increases in the 0.30-carat ones reflect a shift in the market.

The upturn began in the last week of March and accelerated from around April 10. The strongest trends were in D, VS2, prices of which grew 6.3% between April 1 and May 12, and F, VVS2, which saw a 5.9% increase.

Lower supply was a major driver. The number of round, 0.30-carat, D to H, internally flawless to VS2 diamonds on the platform slid 21% between April 1 and May 12 and were down 70% since January 1.

The inventory drop was especially sharp in D to F, internally flawless to VVS goods, which saw a 51% decline in stone count as of May 1 compared with the average of the previous three months.

Manufacturers had focused their production cuts on these areas because of an oversupply throughout 2025.

VS1 diamonds with D to H color recorded a 32% decline in the number of stones over the April 1 to May 12 period, according to Rapaport Trade data.

The stone count for D to H, VVS2 diamonds fell 26% for the same period, with D to F inventory in that clarity slumping 33%.

Dealers also report growing demand from European brands and global retailers for 0.30-carat collection goods in the past two months.

“It is the main demand from a few high-end brands, and their numbers are up from last year,” said an Antwerp-based supplier of smaller diamonds to European brands. “On the other hand, demand in 0.50 carats [and] up from [the] same customers is down.”

The increases are a modest correction following last year’s price crash in small sizes. The Rapaport Trade Diamond Index (RAPI™) for 0.30-carat diamonds, which tracks round, D to H, internally flawless to VS2 goods, plummeted 20.3% in 2025 and slipped a further 1.4% in the first three months of 2026.

This background might explain why buyers are in the market for 0.30-carat diamonds. The goods are relatively inexpensive right now, enticing big brands and other jewelers to purchase them for fashion jewelry. This rush coincided with rock-bottom availability, putting upward pressure on prices. The episode confirms that what goes down must, to an extent, come up.

Main Image : David Polak.

READ FULL REPORT HERE

Source : Rapaport